When it comes time to close a business in Virginia, many business owners feel uncertain about the steps they should take to safeguard their own interests.

For this reason, many will look for advice on how to best close out their business in a way that minimizes their personal liabilities and obligations.

However, while the process may seem daunting at first (especially since every business is different), the general procedures you'll follow are standardized across industries.

In most cases, you'll have to follow three steps to close a business in Virginia:

- Vote and Make Plans to Dissolve the Business — Officially vote or determine to dissolve your business. Then, make a plan to pay and clear any and all outstanding debts, liabilities, and obligations.

- Wind Up Your Business — Take steps to resolve any outstanding issues relating to your business, such as paying any outstanding debts, distributing the business's assets, and closing out any business-owned accounts.

- File Articles of Cancellation with the Virginia SCC — After you finish winding up all the loose ends, you can file a short form with the Virginia State Corporation Commision (SCC) to officially close your business.

As you can see, closing a business generally follows a relatively simple process.

Namely, (1) decide on the manner in which you want to dissolve your business, as outlined in your operating agreement or bylaws, (2) resolve any outstanding debts, obligations, or requirements to effectively "zero out" the business's assets and liabilities, and (3) formally tell the SCC that you've finished the wind-up process and file any required paperwork.

We'll outline the basics of this process below.

However, keep in mind that winding up a business is often a difficult process, so it's wise to speak to both an attorney and an accountant before you begin the formal dissolution process.

Contents

- How to Dissolve an LLC in Virginia

- Winding Up Your Business

- Filing Your Articles of Cancellation with the Virginia SCC

- How to Close a Business in Virginia FAQ

- Key Takeaways

How to Dissolve an LLC in Virginia

The first step in closing your business is getting the go-ahead from all of (or a majority of) the business's members and owners.

To begin, you'll have to decide whether you want to close the business, sell the business, transfer your ownership to another party, or file for bankruptcy and liquidate the business's assets.

Put another way, what is your goal for separating yourself from the business?

Do you want to close it because it isn't profitable enough and you want your equity back? Do you want to end a business partnership over a disagreement? Are you in dire straights and in need of fast cash to pay back creditors?

Figuring out your "out" is often one of the most important steps to dissolving a business, as it lays out the next steps you should take in your case.

For example, there's no point in dissolving a business if you could instead sell it to another party for a healthy profit.

Similarly, transferring ownership to a partner or close family member could be as easy as a quick buy-out agreement.

Finally, dissolving your business as a part of a bankruptcy filing is outside the scope of an article such as this, or really any article you'll find online, and is generally something you'll want to speak to an attorney about in person.

With these three cases out of the way, we are left with the relatively basic "I simply want to close my business for personal reasons" angle.

The point, then, is that there are a variety of ways to distance yourself from a business, and taking steps to close the business is just one strategy you might want to pursue to meet your goals.

While we'll outline the basics of this process below, it's always wise to consider all your options before you jump to closing down the business as a whole.

Follow Your Operating Agreement

In cases where owners want to dissolve their business, they'll usually have to follow the steps for dissolution outlined in their operating agreement or bylaws.

As a few common topics to consider that are often included in these documents, you may have to:

- Hold a vote between all the business's members and owners to dissolve the business.

- Get written permission of all members and owners to dissolve the business.

- Determine a formal date of dissolution and the action plan leading up to that date.

- Figure out a plan for distributing the business's assets to members, owners, and creditors.

- Figure out a plan for closing out the business's accounts.

While this is far from an exhaustive list, the general gist of the matter is that your operating agreement or bylaws should lay out the steps you need to take to formally decide on an action plan for dissolving your business.

In general, however, this step will center around getting permission to dissolve the business via either a vote OR the collection of written permission from all the business's members.

Winding Up Your Business

Winding up your business generally involves liquidating as much as possible and then distributing any assets to creditors and owners of the business, as outlined in the Virginia Code.

Once you (and your co-owners if applicable) have decided to dissolve the business, the next step is to take action to meet all of Virginia's requirements for winding up your affairs.

There are two key resources we can use to simplify this process: Form LLC1050, Articles of Cancellation of a Virginia LLC, and Virginia Code § 13.1-1049.

From the articles of cancellation form (which you will file at the end of the process), we can learn that:

The company must wind up its affairs before filing these articles (of cancellation). The company must pay and clear, or arrange to pay and clear, all its debts, liabilities, and obligations. Then, it must distribute the remaining property and assets to its members.

Specific Instructions, Article IV Winding Up of Affairs | Form LLC1050, Articles of Cancellation of a Virginia LLC See also Va. Code § 13.1-1048. Winding up.

Then, from Virginia Code § 13.1-1049, the section on distributing assets, we learn that:

Upon the winding up of a limited liability company, the assets of the limited liability company shall be distributed as follows:

1. To creditors, including members who are creditors, to the extent permitted by law, in satisfaction of the liabilities of the limited liability company [and] other than for distributions to members;

2. Unless otherwise provided in the articles of organization or an operating agreement, to members and former members in satisfaction of liabilities for distribution; and,

3. Unless otherwise provided in the articles of organization or an operating agreement, to members first for the return of their contributions and second with respect to their interests in the limited liabilities company, in the proportions in which the members share in distributions.

Va. Code § 13.1-1049. Distribution of assets upon dissolution.

Interpreting the Statutory Requirements

We can extract a few key insights from these two quotes.

First, there is a specific legal process through which you must wind up your business. Namely:

- Pay and clear all debts, liabilities, and obligations to any creditors (including members who are creditors), including taxes, bank debt, and any outstanding invoices against your company (note that this includes providing written notice of your business's dissolution to any outstanding creditors, as well as a deadline of no less than 120 days for the creditor to confirm the validity of the liability claim);

- Distribute any remaining funds to members and former members in satisfaction of liabilities for distribution (such as if a former partner took out a loan on behalf of or for the company);

- Finally, any remaining funds could then be distributed to the current members for any contributions they have made to the business and then with respect to their proportion of ownership in the company.

Second, and more importantly, outside of these three factors, the Virginia Code actually doesn't provide any other specific requirements for winding up a company.

The actual process you follow (outside of the ordered list above) can largely be based on the specific legal strategy you choose to follow at the advice of your attorney and accountant.

For example, in addition to the three legal processes outlined above, you may also want to perform actions such as:

- Placing a public notice of dissolution in a newspaper to prove notification in the event someone sues the business after it is formally dissolved.

- Notify any agencies or organizations that handle your business's state licensing and permits, as you may have to take proactive steps to terminate your business license.

- Close all bank accounts and other accounts related to your business after the distribution process is finished.

After you finish winding up your business by distributing all remaining assets to creditors and members, closing out all accounts and other liabilities related to the business, and generally "closing up shop," you can take the final step of filing your articles of cancellation with the Virginia SCC.

Filing Your Articles of Cancellation with the Virginia SCC

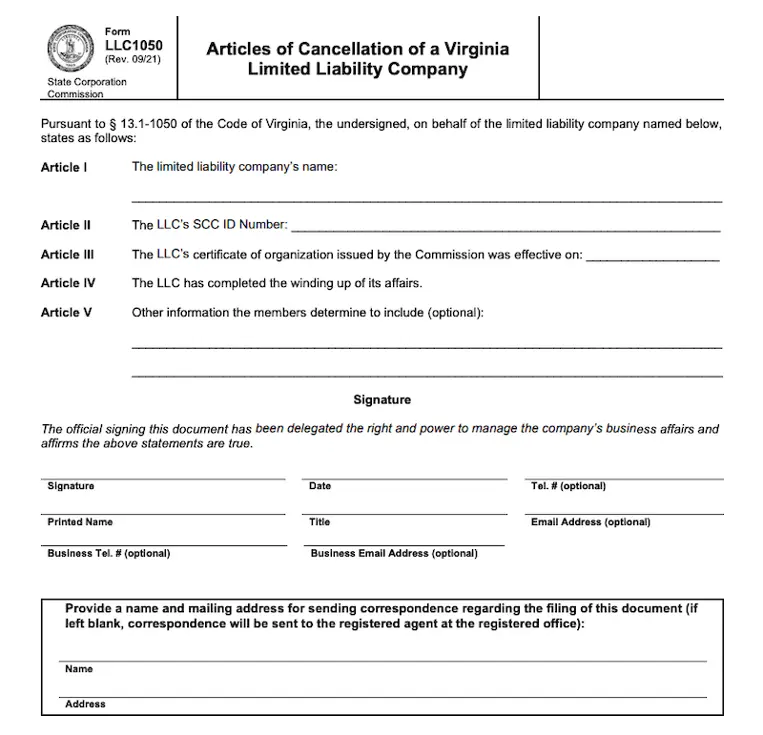

An example screenshot of Form LLC1050, Articles of Cancellation of a Virginia LLC, taken May 10, 2022. This is the form you will file at the end of the winding up process if you want to dissolve an LLC.

Filing your articles of cancellation is actually relatively simple once you've finished winding up your business.

Generally speaking, all you'll have to do is fill out Form LLC1050, Articles of Cancellation of a Virginia Limited Liability Company (or the applicable form found on the SCC's website for your entity type) and then either mail the physical form in or submit it online through the SCC's Clerk's Information System website.

It will cost somewhere in the range of $10 to $25 to file most forms relating to closing a business, and it will generally take the SCC around a week or two to process your paperwork.

Ongoing Requirements After You Dissolve Your Business

As one final note, please keep in mind that you should take steps to preserve your records after the dissolution of your business in the event you have to face a lawsuit or inquiry in the future.

Generally speaking, it's wise to keep records of valuable property (such as equipment, vehicles, or real estate) for several years, as well as any employee tax records for at least four years.

You may also want to hold onto any records of your business's legal state at the time of the dissolution of your business.

For example, keeping a record of your Articles of Organization and a copy of your articles of cancellation may be helpful in the event a partner or creditor attempts to sue for an outstanding liability after the dissolution of your company.

How to Close a Business in Virginia FAQ

Closing a business can be incredibly case-specific, so it's wise to consult with a professional if you have any doubts about your path forward.

Is there a filing fee to close a business in Virginia?

Yes. The filing fee to close a Virginia LLC is $25, and the filing fees for closing other legal entities generally fall somewhere close to this value.

Do I need to hire an attorney or an accountant to help me close my business?

For sole proprietorships and other simple business entities (or businesses that have yet to do business), the answer is generally no, as the limited number of assets to divide (and creditors to account for) makes the process relatively simple.

In almost every other case, it's generally wise to at least speak with an attorney and/or an accountant to make sure you're making the best decision for your specific situation.

Because of the significant risks involved (generally in regards to unpaid creditors) it's smart to take the time to close your business the right way rather than having to face the risk of litigation down the road.

What does it mean to "wind up" my business's operations?

"Winding up" a business is generally defined as a shift in the business's purpose from "making money" to "paying off creditors and distributing assets."

Put another way, winding up a business refers to the transitional phase between when the business decides to close its doors and when it formally finishes distributing all of its assets to creditors and other interested parties.

The term is synonymous with "liquidating" a business, which means that all of the business's assets are converted to cash as a way of paying off any and all liabilities and paying out any remaining equity the owners might have in the business.

How long does it take to close my business?

Generally speaking, it will take you roughly one to two weeks plus the time it takes to wind up your business's operations.

Or, put another way, the time it takes to close your business will generally be either (1) how long it takes to pay off any creditors and cease operations, or (2) an amount of time no less than 120 days, due to the "known claims" requirement for notice given to creditors, as outlined in the Virginia Code.

How long do I have before someone can use my former business name?

Any other person or entity can file to claim your former business name from the moment the Virginia SCC accepts your articles of cancellation.

Note, however, that if you filed for a trademark using your prior business name those protections may still apply.

What happens if I don't formally dissolve my business with the SCC?

All Virginia businesses must file an annual report and pay a fee to renew their business registration with the Virginia SCC.

If a business fails to file their annual report, it will no longer be in good standing with the SCC. Four months after being designated as such, the SCC will automatically revoke the corporation's certificate of authenticity and formally consider the business to be abandoned and dissolved.

Note, however, that there is a difference between formal registration with the SCC and the various obligations and liabilities owed by the business (and its owners) to creditors and other institutions.

While the SCC may formally revoke your business's registration, the various banks and other creditors that your business owes money to will still likely hold your business (and, potentially, you) liable for any outstanding debts.

Key Takeaways

Closing a business generally occurs in three steps: (1) voting to dissolve the business and making a plan, (2) winding up the business's operations by distributing all assets to creditors and owners, and (3) submitting some paperwork to the Virginia SCC.

Generally speaking, it's relatively easy to close a business in Virginia, provided you take the time to coordinate with an attorney and an accountant during the process.

In most cases, closing your business will be a three-step process:

- Vote and Make Plans to Dissolve the Business — Officially vote or determine to dissolve your business. Then, make a plan to pay and clear any and all outstanding debts, liabilities, and obligations.

- Wind Up Your Business — Take steps to resolve any outstanding issues relating to your business, such as paying any outstanding debts, distributing the business's assets, closing out any business-owned accounts, etc.

- File Articles of Cancellation with the Virginia SCC — After you finish winding up all the loose ends, you can file a short form with the Virginia State Corporation Commision (SCC) to officially close your business.

Note, however, that while the process may seem simple at first, there are numerous pitfalls to watch out for in regards to your personal liability.

For example, you will have to account for your business's tax obligations, member distribution, and a variety of other hidden requirements that may make the process difficult depending on your particular situation.

For this reason, it's highly recommended that you speak with both an attorney and an accountant about your business plans before you choose to close up shop.

Only an experienced professional who has reviewed your entire case can give you the insight you need to safely and quickly close your business and reclaim any equity that might be left over after you pay your outstanding liabilities.

Further Reading

- 11 Ways an Attorney Can Help you Start a Small Business in Virginia

- "Doing Business As" (DBA) Registration in Virginia

- How to Start a Business in Virginia: A 10-Step Guide

- Virginia Business Structures Explained: LLCs, Corporations, and More

- Virginia LLC Tax Filing Requirements: How LLCs Pay Their Taxes

Other Resources

- Virginia Code § 13.1-1048. Winding up. — The Virginia Code section that describes the basics of the winding up process.

- Virginia Code § 13.1-1049. Distribution of assets upon dissolution. — The Virginia Code section that describes how assets should be distributed upon the dissolution of a business.

- Forms and Fees | Virginia SCC — The page where you can find the specific forms (and their related fees) for closing every type of business entity in Virginia.

- Form LLC1050, Articles of Cancellation of a Virginia Limited Liability Company — The specific form for closing a Virginia LLC.

- Close or Sell Your Business | U.S. Small Business Administration — A page by the SBA on the different ways an owner can close or separate themselves from a business.

- Closing a Business | IRS — A page by the IRS on your tax obligations when closing a business. It also provides additional information and general advice on how to go through the process.